On 18 January 2024, our Founder and CEO, Gilbert Verdian, called on UK asset managers to take the lead in programmable payments during a webinar in partnership with The Investment Association.

The webinar, entitled ‘Which form of digital money will power future digital markets?’, was hosted by the IA’s Head of Innovation & Operations, John Allen. Gilbert gave his perspective on how and why traditional financial services are becoming increasingly digital, with the introduction of tokenised deposits, central bank digital currencies and stablecoins.

Gilbert began by touching on the evolution of blockchain in the UK, “as a country, we looked at it quite early from a policy perspective, but it was too early to truly understand the technology and the market” he said, “fast forward to 2024, it is now institutional and it’s driving a fundamental change in financial services.”

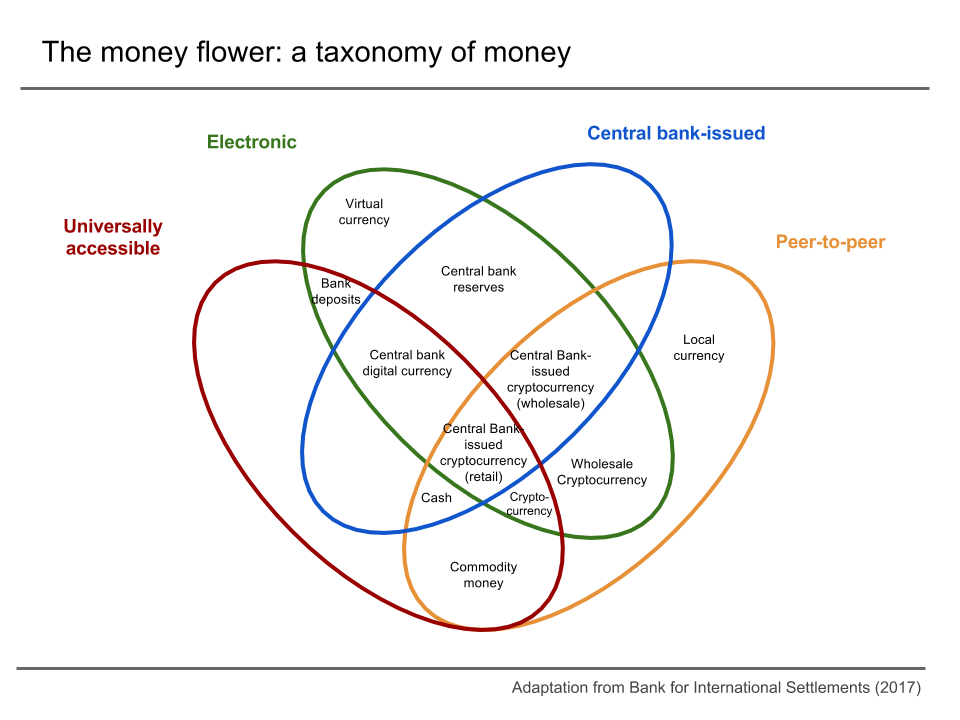

He went on to explore the interdependencies between assets and demonstrated using the ‘money flower’, a diagram by the Bank for International Settlements, he showcased the current forms of money, how they differ and where we can overlay new forms of money within the existing system. He said, “a lot of blockchain concepts are not about complete disruption of the financial system, it should complement what we have within the financial services industry”, before moving onto another diagram that showed how digital money can fit within the existing system, as a unit of account, a medium of exchange and a store of value.

He clarified a concept that many misunderstand, “money itself is not digital, although we have digital bank accounts, that money is electronic” however, “the new form of money is digital – this is where CBDCs and tokenised bank liabilities come in.”

Gilbert moved on to discuss our recent CBDC work with the Bank of England on Project Rosalind, which sought to provide answers to these questions: what is different about digital money, why is it needed and what does it look like for the ecosystem? He added that the project set out to design what digital money could look like, “we built the backend infrastructure and technology stack to explore specific use cases such as payments and complex workflows.”

He then shared some of the key lessons from the project, starting with a diagram of what the new infrastructure would typically look like and what the industry could do with it. “We created something that is future-proof, removes friction around payments and provides the flexibility needed for the industry to innovate”, he added “for the first time, the central bank will be able to offer a new form of money for most participants who are regulated to have access to it.”

According to Gilbert, one of the biggest breakthroughs during the project was answering the question, what is the difference between a digital pound and a normal pound? “The answer came from the power of smart contracts, by creating multi-party locks that add programmability to money through tokenisation”, he said “they are unique to this form of money and enable the locking and release of funds conditioned by the authorisation of a third party.”

But what does this mean for asset managers in the UK? Gilbert believes it will provide “the ability to use this new form of money to have real-time atomic settlements – reducing risks in transactions, driving operational efficiencies and offering access to new pools of liquidity.”

The next part of the webinar focused on the opportunity for tokenisation. He explained that we’re witnessing a move towards the tokenisation of different asset classes, from real estate and commodities to funds and individual securities, “there is a real appetite for tokenisation, driven by a motivation to access new capital, increase liquidity and improve efficiency – there’s also the potential for huge savings.”

To conclude, Gilbert shared his vision for the industry, “a new market of transformed digital assets is being developed”, he added “these digital assets are tokenised, interoperable new instruments.” This led onto his final point, “evolving money into a digital form will offer 24/7 transacting and trading, greater access to liquidity, all whilst removing friction, reducing risk and shrinking costs.” And this is something that he believes the UK is best placed to lead on, “the industry, our expertise and our history means that we have the facilities to shape what the next generation financial system should look like.”

How Quant can help